Image courtesy of Arlanxeo Singapore

“In the first quarter of 2023, we were watching the beginning of a slowdown in raw material prices. This trend has carried on through the year, recovery seemingly ‘one quarter away’ until that quarter passed,” said Aaron Montgomery, president and CEO of Ouray, an emergency response service company for chemical manufacturers and chemical tankers.

Montgomery describes the unfulfilled hope that the commodity chemical markets have held on to ever since demand started to weaken towards the end of 2022, leaving the industry submerged in oversupply. As much as we would like to report the later quarters of this year will bring the relief the industry so desperately needs, we are about to relate why this is unlikely to be the case. If the answer had to be reduced to one word, it would be China.

The Southeast Asian chemical industry is to see ferociously more competition, both at home and in its primary export market, China, as demand remains languid and supply is strong, particularly from the Middle East. Southeast Asia is not only a feedstock net importer but also export-focused, a dangerous combination of dependencies that weakens its grip on the market. To make matters worse, most of the local crackers are naphtha-based, subjecting the industry to oil price volatility.

“Elevated oil prices have meant very narrow conversions for the players in SEA. Last year some of our customers turned off their plants, and some even preferred to sell the naphtha feedstock in the spot markets rather than converting it to olefins,” explained Ubolrat Wiwattanakul, vice president for Southeast Asia at Lummus Technology, a technology licensor that has worked on some of the largest projects in the region, including PrefChem’s petrochemical complex in Malaysia, Thai Oil’s clean fuel or Braskem & SCG’s ethanol-to-ethylene projects in Thailand.

Wiwattanakul said many plants in the region have yet to return to full capacity since the pandemic. Analysts anticipate this is only the beginning of more serious production cuts and permanent closures in naphtha-dependent regions, which have been running on negative margins. Global operating rates for both ethylene and propylene, the two main building blocks for petrochemical products, are expected to decline to 80% and 71% between 2022-2030, down 8% and 9% from the 2000-2001 period, according to ICIS. Loss-making petrochemical companies have pushed through with hopes of a flare-up in prices, but this prospect does not look likely due to slow demand. China has been the engine of growth for petrochemical demand, delivering demand growth for chemicals at 6-8% per year; however, future projections are much more subdued, forecasted at 1-3% by ICIS. This is causing a “demand recession,” as described by Swiss-based consultancy New Normal.

Roger Marchioni, business director for Braskem Asia and managing director of newly formed Thai company Braskem Siam, a JV with SCG, also sees impending closures in the polyolefin space, one of the most affected in the current downcycle: “The polyolefins space has been very slow, forcing the industry to do some serious homework in marking out profitable assets from those that are not, and making difficult decisions accordingly to rationalize production. This has happened before, but in a shy kind of way, yet today, we see firm action across Europe, Northeast Asia, and even Southeast Asia. On the other hand, the US and the Middle East remain quite competitive.”

Even at a lower growth rate, China remains a very large demand base for petrochemicals, a base that it wants to self-serve. 10 years ago, China announced its self-sufficiency goals in the petrochemical sector and it has rigurously followed them through. In the olefin market, the International Energy Agency estimates that China makes up for over half of all new olefin capacity between 2022 and 2028. ChemOrbis reports Chinese plans to introduce 7.5 million tpa of polyethylene (PE) this year, and a further 6.7 million tpa in 2025. That would mean China’s self-sufficiency level in PE is to reach about 70% this year. Polypropylene (PP), the second most used polymer, is already reaching parity at about 96%, according to ICIS. If capacity additions follow at the same rate, China could turn into a net PP exporter in the next few years.

ICIS also informs that China has turned from a purified terephthalic acid (PTA) importer, importing about 6.6 million tpa in 2010, into a net exporter, at 3.3 million tpa in 2022. The same drastic transition from importer to exporter also took place in the polyester fibers, polyethylene terephthalate (PET) bottle grades, and polyvinyl chloride (PVC). The shift is extreme. China used to be the world’s biggest net importer of PET and polyester fibers. Now it is the largest net exporter. China’s 2026-2030 five-year national plan targets self-sufficiency in other chemical value chains. Experts think this would be possible in high-density polyethylene (HDPE), low-density PE (LDPE), and linear-low-density PE (LLDPE). In the styrene monomer market, China is also close to self-sufficiency. Some venture to report that monoethylene glycol (MEG) and eventually paraxylene could be next.

China is leveraging its coal abundance to make petrochemicals at lower prices compared to its ethane or naphtha-based peers, like Southeast Asia. With coal prices coming down from their peaks in 2022, the coal-to-methanol-to-olefins engine has returned to force. The methanol-to-olefins (MTO) is the largest market for methanol globally, informs Mark Berggren, founder and managing director of Methanol Market Services Asia (MMSA), a global intelligence company for the methanol industry worldwide. “The MTO sector takes almost 20% of the olefins supply to China. It is a strategic industry for China and olefin producers from methanol are currently making small but positive cash margins. Unlike naphtha-based olefin products, which depend on a refinery, MTO producers have much greater flexibility, and are able to buy methanol and manufacture polymers and olefin derivatives on-purpose, whenever needed. This gives the MTO ‘machine’ a significant advantage,” Berggren detailed.

With the world’s hottest petrochemical market no longer needing imports, Southeast Asia is not only left without a principal export outlet, but it also becomes an attractive import target. In the highly oversupplied high-density polyethylene (HDPE) market, where capacity is exceeding demand by around 12 million tpa at operating rates of 79% between 2020-2030, Southeast Asia is projected to represent the second-biggest “prize,” after China itself, which will still account for 37% of the world’s HDPE imports. Southeast Asia will be behind at 24%. That could change should China accelerate its domestic capacity in this segment too.

Besides China, Southeast Asian players are also squeezed by Middle Eastern producers venturing further into the deep-sea APAC markets. “Due to its geographical positioning, Southeast Asia is exposed to imports not only from China, where surpluses of intermediates have built up on account of a slower Chinese economy, but also from the Middle East and the US Gulf Coast. Tariffs between the US and China turned both countries towards Southeast Asia, so the region has become a sort of ‘catch-all’ market for petrochemicals. That poses challenges for domestic producers, who are losing significant market share to lower importers,” explained Thomas Luedi, senior partner and head of Asia Chemicals and commercial excellence practices at global consultancy Bain & Company.

The one player that has made aggressive inroads in APAC is Saudi Arabia’s supermajor, Aramco. After becoming a 50% partner in Petronas’ largest petrochemical complex and flirting with a potential investment in Vietnam, Saudi Aramco sank its teeth into large-scale projects in both South Korea and China. Its subsidiary, S-Oil, is building a 1.8 million tpa ethylene capacity at the Shaheen project in South Korea, to be ready by 2026. Sabic, owned under Saudi Aramco, has also recently announced a US$6.4 billion investment in a 1.8 million tpa cracker in Fujian, China, to be completed in 2026. Aramco’s subsidiary AOC also took a small (10%) stake in Rongsheng Petrochemical, the largest privately owned petrochemical company in China, as well as another 10% equity stake in Hengli Petrochemical. Saudi Aramco and Total Energies are progressing with the mixed-feed 1.7 million tpa (ethylene) Admiral project, planned to start in 2027. Supply in other Middle Eastern countries is also picking up. In the UAE, Borouge is building the world’s largest single-site polyolefin complex.

Petrochemical investments by Middle Eastern players, whether at home or in other markets, are closely watched because the region is expected to divert its abundant oil into petrochemical products, as demand for fuels will eventually decline due to the electrification and decarbonization of the transport sector. In a press release, Aramco said the company could convert up to 4 million bbl/day of liquids into chemicals by 2030. The crude-to-oil-to-chemicals (COTC) is a new concept and a possible way for the Middle East to protect its most vital resource, oil, by shifting more to petrochemicals. Petrochemicals are believed to be the biggest driver for oil demand in coming decades, according to the IEA. Superior cost-per-ton economics in the Middle East could displace current petrochemical players in Southeast Asia, or risk sending the entire market into a long-lasting oversupply.

Fluid catalytic cracker (FCC), using naphtha and aromatics from FFC gasoline as feedstocks for petrochemicals like olefins, is the most known technology in the crude-to-chemical space. Aramco’s subsidiary in Korea, S-Oil, is one of the first to have commercialized the technology. Projects in China including Hengli Petrochemical and Zhejiang Petroleum and Chemicals (ZPC) also use it, having achieved up to 45% conversion rates per barrel of oil, much more than the usual 10% produced in regular refineries. Aramco is working to push the conversion rate to 70-80%. In a more direct diversification to petrochemicals, Abu Dhabi National Oil Company’s (ADNOC) has placed a bid on German specialty chemicals producer, Covestro, but the offer was reportedly rejected. ADNOC then proceeded to show interest in the Brazilian leading PE company, Braskem.

Southeast Asian petrochemical companies could also turn to more crude-to-chemicals in theory, but it will be hard to compete with the large scale of the new plants built in China and the Middle East. Also, with gasoline prices in a much better shape compared to olefin prices, Southeast Asian refiners have little incentive to invest in conversions. For now, the industry is focused on survival, making “tweaks” to current plants to mitigate negative margins in saturated products. “Producers are not making large investments, but they are looking at ways to modify their plants to make products with better yields. For instance, if the C3 market is doing very poorly, we can deploy our olefins conversion technology to produce other products. Southeast Asian companies are not young producers anymore, but in the global market, they remain newcomers,” said Ubolrat Wiwattanakul, vice president for Southeast Asia at Lummus Technology.

Cost-optimization and efficiency programs are also high on the agenda of petrochemical players in the region. At the high end of this, successful value enhancement programs have led to huge savings. Thai-based PET leader Indorama Ventures’ “Project Olympus” delivered over US$600 million in cost savings. Similarly, Borouge, a JV between ADNOC and Austria’s Borealis, also delivered US$607 million in positive EBITDA as part of its Value Enhancement Program.

On the M&A front, transactions that match feedstock with the market, potentially from the Middle East into Asia, are likely. The recent acquisition by Thai-Indonesian Chandra Asri, in JV with Glencore of Shell’s refinery in Singapore is one example of intra-regional investment that could give Indonesia’s only naphtha cracker better access to feedstock via Singapore. According to Thomas Luedi, leading Asia chemicals and commercial excellence practices for Bain and Company, standalone (or non-integrated) crackers are the most vulnerable in the current environment and will continue to face challenges, whereas crackers integrated back to refineries have a better cost position. That incentivizes non-integrated crackers to look for feedstock options.

With naphtha prices on a downward trend, futures trading at about US$660/ton, and contract net transaction prices at about half that range, Southeast Asian petrochemical producers should see marginal improvements in the near term. However, the long-term view is uncertain with overcapacities in the olefin space threatening the prices of petrochemicals and expectations that oil and refining could potentially play a bigger role in petrochemicals. A second wave of mainland Chinese naptha crackers is taking shape, writes Chemical Markets Analytics (Dow Jones company). This is primarily led by state-owned enterprises. The new supply could send the ethylene market into oversupply.

Between 1995 and 2020, the chemical industry grew more slowly (175%) than the world GDP (149%), according to the Information Technology and Innovation Foundation (ITIF), a think tank. The correlation between GDP and chemicals has historically been a close one, but this may no longer be the case, the energy transition pressurizing both the oil and gas and chemical sectors to prepare for a lower-carbon future. That makes demand uncertain, especially for countries relying heavily on exports to China, like Singapore and Thailand, whereas Indonesia and Vietnam remain busy with their under-supplied domestic sector. It will be interesting to see whether more petrochemical complexes in these two countries could make sense in light of capacity additions elsewhere.

One thing that Southeast Asian countries could learn from China is investing beyond quarterly performance. China has invested during “sickness and health,” driven not solely by profits, but by the longer-term prospects of job creation, stability, and advancing market positions when others were preoccupied with overheads or paused to mend the wounds of past and present challenges. Of course, few have the luxury of subsidies, scale, and integration with a humongous manufacturing sector that China grants, but there are still many spots to fill in specialty chemicals before China catches up to those too.

China is currently in a situation of “low-end surplus, high-end shortage,” which means it has excess or severe excess supply of up to 75% by 2025 in petrochemical products, but it still has to import 50% of its higher-end chemicals, as found by German newspaper CheManager International. With the capacity-demand ratio growing in basic chemicals like ethylene oxide or PTA forcing a reduction in Chinese utilization rates, in 2021 China issued the ”Market Access Negative List” to restrict new chemical projects in saturated areas like ethylene, p-xylene, and coal-to-olefins and coal-to-paraxylene projects, directing its focus on the higher-value markets, including synthetic materials, functional materials or electronic chemicals. China is the largest consumer of specialty chemicals in the world, but it could be a matter of time before the country starts tackling this gap.

In the meantime, the country that is bringing the most hope for petrochemical makers is India, whose demand for PE and PP is on an upward trend, according to S&P statistics. However, competition to serve this hungry sector will be cutthroat, and Southeast Asian companies do not have the upper hand on costs.

Ubolrat Wiwattanakul, leading Southeast Asia for Lummus Technology, leaves us with the concluding thought for this article: “People used to think in cycles before, but there are bigger things on the horizon now – conflicts, oil crises, shifting geopolitics – all overwriting supply-to-demand fundamentals. The Southeast Asian petrochemical industry has the fighting spirit to invest in its population. If the regional industry operates only in the low-cost arena, there is always going to be a new player producing cheaper.

Image courtesy of Arlanxeo Singapore

“In the first quarter of 2023, we were watching the beginning of a slowdown in raw material prices. This trend has carried on through the year, recovery seemingly ‘one quarter away’ until that quarter passed,” said Aaron Montgomery, president and CEO of Ouray, an emergency response service company for chemical manufacturers and chemical tankers.

Montgomery describes the unfulfilled hope that the commodity chemical markets have held on to ever since demand started to weaken towards the end of 2022, leaving the industry submerged in oversupply. As much as we would like to report the later quarters of this year will bring the relief the industry so desperately needs, we are about to relate why this is unlikely to be the case. If the answer had to be reduced to one word, it would be China.

The Southeast Asian chemical industry is to see ferociously more competition, both at home and in its primary export market, China, as demand remains languid and supply is strong, particularly from the Middle East. Southeast Asia is not only a feedstock net importer but also export-focused, a dangerous combination of dependencies that weakens its grip on the market. To make matters worse, most of the local crackers are naphtha-based, subjecting the industry to oil price volatility.

“Elevated oil prices have meant very narrow conversions for the players in SEA. Last year some of our customers turned off their plants, and some even preferred to sell the naphtha feedstock in the spot markets rather than converting it to olefins,” explained Ubolrat Wiwattanakul, vice president for Southeast Asia at Lummus Technology, a technology licensor that has worked on some of the largest projects in the region, including PrefChem’s petrochemical complex in Malaysia, Thai Oil’s clean fuel or Braskem & SCG’s ethanol-to-ethylene projects in Thailand.

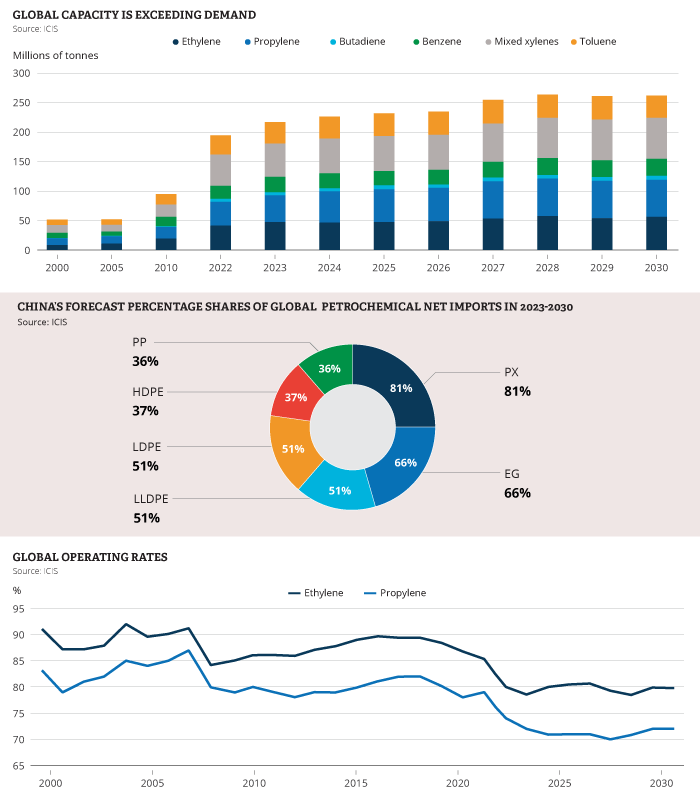

Wiwattanakul said many plants in the region have yet to return to full capacity since the pandemic. Analysts anticipate this is only the beginning of more serious production cuts and permanent closures in naphtha-dependent regions, which have been running on negative margins. Global operating rates for both ethylene and propylene, the two main building blocks for petrochemical products, are expected to decline to 80% and 71% between 2022-2030, down 8% and 9% from the 2000-2001 period, according to ICIS. Loss-making petrochemical companies have pushed through with hopes of a flare-up in prices, but this prospect does not look likely due to slow demand. China has been the engine of growth for petrochemical demand, delivering demand growth for chemicals at 6-8% per year; however, future projections are much more subdued, forecasted at 1-3% by ICIS. This is causing a “demand recession,” as described by Swiss-based consultancy New Normal.

Roger Marchioni, business director for Braskem Asia and managing director of newly formed Thai company Braskem Siam, a JV with SCG, also sees impending closures in the polyolefin space, one of the most affected in the current downcycle: “The polyolefins space has been very slow, forcing the industry to do some serious homework in marking out profitable assets from those that are not, and making difficult decisions accordingly to rationalize production. This has happened before, but in a shy kind of way, yet today, we see firm action across Europe, Northeast Asia, and even Southeast Asia. On the other hand, the US and the Middle East remain quite competitive.”

Even at a lower growth rate, China remains a very large demand base for petrochemicals, a base that it wants to self-serve. 10 years ago, China announced its self-sufficiency goals in the petrochemical sector and it has rigurously followed them through. In the olefin market, the International Energy Agency estimates that China makes up for over half of all new olefin capacity between 2022 and 2028. ChemOrbis reports Chinese plans to introduce 7.5 million tpa of polyethylene (PE) this year, and a further 6.7 million tpa in 2025. That would mean China’s self-sufficiency level in PE is to reach about 70% this year. Polypropylene (PP), the second most used polymer, is already reaching parity at about 96%, according to ICIS. If capacity additions follow at the same rate, China could turn into a net PP exporter in the next few years.

ICIS also informs that China has turned from a purified terephthalic acid (PTA) importer, importing about 6.6 million tpa in 2010, into a net exporter, at 3.3 million tpa in 2022. The same drastic transition from importer to exporter also took place in the polyester fibers, polyethylene terephthalate (PET) bottle grades, and polyvinyl chloride (PVC). The shift is extreme. China used to be the world’s biggest net importer of PET and polyester fibers. Now it is the largest net exporter. China’s 2026-2030 five-year national plan targets self-sufficiency in other chemical value chains. Experts think this would be possible in high-density polyethylene (HDPE), low-density PE (LDPE), and linear-low-density PE (LLDPE). In the styrene monomer market, China is also close to self-sufficiency. Some venture to report that monoethylene glycol (MEG) and eventually paraxylene could be next.

China is leveraging its coal abundance to make petrochemicals at lower prices compared to its ethane or naphtha-based peers, like Southeast Asia. With coal prices coming down from their peaks in 2022, the coal-to-methanol-to-olefins engine has returned to force. The methanol-to-olefins (MTO) is the largest market for methanol globally, informs Mark Berggren, founder and managing director of Methanol Market Services Asia (MMSA), a global intelligence company for the methanol industry worldwide. “The MTO sector takes almost 20% of the olefins supply to China. It is a strategic industry for China and olefin producers from methanol are currently making small but positive cash margins. Unlike naphtha-based olefin products, which depend on a refinery, MTO producers have much greater flexibility, and are able to buy methanol and manufacture polymers and olefin derivatives on-purpose, whenever needed. This gives the MTO ‘machine’ a significant advantage,” Berggren detailed.

With the world’s hottest petrochemical market no longer needing imports, Southeast Asia is not only left without a principal export outlet, but it also becomes an attractive import target. In the highly oversupplied high-density polyethylene (HDPE) market, where capacity is exceeding demand by around 12 million tpa at operating rates of 79% between 2020-2030, Southeast Asia is projected to represent the second-biggest “prize,” after China itself, which will still account for 37% of the world’s HDPE imports. Southeast Asia will be behind at 24%. That could change should China accelerate its domestic capacity in this segment too.

Besides China, Southeast Asian players are also squeezed by Middle Eastern producers venturing further into the deep-sea APAC markets. “Due to its geographical positioning, Southeast Asia is exposed to imports not only from China, where surpluses of intermediates have built up on account of a slower Chinese economy, but also from the Middle East and the US Gulf Coast. Tariffs between the US and China turned both countries towards Southeast Asia, so the region has become a sort of ‘catch-all’ market for petrochemicals. That poses challenges for domestic producers, who are losing significant market share to lower importers,” explained Thomas Luedi, senior partner and head of Asia Chemicals and commercial excellence practices at global consultancy Bain & Company.

The one player that has made aggressive inroads in APAC is Saudi Arabia’s supermajor, Aramco. After becoming a 50% partner in Petronas’ largest petrochemical complex and flirting with a potential investment in Vietnam, Saudi Aramco sank its teeth into large-scale projects in both South Korea and China. Its subsidiary, S-Oil, is building a 1.8 million tpa ethylene capacity at the Shaheen project in South Korea, to be ready by 2026. Sabic, owned under Saudi Aramco, has also recently announced a US$6.4 billion investment in a 1.8 million tpa cracker in Fujian, China, to be completed in 2026. Aramco’s subsidiary AOC also took a small (10%) stake in Rongsheng Petrochemical, the largest privately owned petrochemical company in China, as well as another 10% equity stake in Hengli Petrochemical. Saudi Aramco and Total Energies are progressing with the mixed-feed 1.7 million tpa (ethylene) Admiral project, planned to start in 2027. Supply in other Middle Eastern countries is also picking up. In the UAE, Borouge is building the world’s largest single-site polyolefin complex.

Petrochemical investments by Middle Eastern players, whether at home or in other markets, are closely watched because the region is expected to divert its abundant oil into petrochemical products, as demand for fuels will eventually decline due to the electrification and decarbonization of the transport sector. In a press release, Aramco said the company could convert up to 4 million bbl/day of liquids into chemicals by 2030. The crude-to-oil-to-chemicals (COTC) is a new concept and a possible way for the Middle East to protect its most vital resource, oil, by shifting more to petrochemicals. Petrochemicals are believed to be the biggest driver for oil demand in coming decades, according to the IEA. Superior cost-per-ton economics in the Middle East could displace current petrochemical players in Southeast Asia, or risk sending the entire market into a long-lasting oversupply.

Fluid catalytic cracker (FCC), using naphtha and aromatics from FFC gasoline as feedstocks for petrochemicals like olefins, is the most known technology in the crude-to-chemical space. Aramco’s subsidiary in Korea, S-Oil, is one of the first to have commercialized the technology. Projects in China including Hengli Petrochemical and Zhejiang Petroleum and Chemicals (ZPC) also use it, having achieved up to 45% conversion rates per barrel of oil, much more than the usual 10% produced in regular refineries. Aramco is working to push the conversion rate to 70-80%. In a more direct diversification to petrochemicals, Abu Dhabi National Oil Company’s (ADNOC) has placed a bid on German specialty chemicals producer, Covestro, but the offer was reportedly rejected. ADNOC then proceeded to show interest in the Brazilian leading PE company, Braskem.

Southeast Asian petrochemical companies could also turn to more crude-to-chemicals in theory, but it will be hard to compete with the large scale of the new plants built in China and the Middle East. Also, with gasoline prices in a much better shape compared to olefin prices, Southeast Asian refiners have little incentive to invest in conversions. For now, the industry is focused on survival, making “tweaks” to current plants to mitigate negative margins in saturated products. “Producers are not making large investments, but they are looking at ways to modify their plants to make products with better yields. For instance, if the C3 market is doing very poorly, we can deploy our olefins conversion technology to produce other products. Southeast Asian companies are not young producers anymore, but in the global market, they remain newcomers,” said Ubolrat Wiwattanakul, vice president for Southeast Asia at Lummus Technology.

Cost-optimization and efficiency programs are also high on the agenda of petrochemical players in the region. At the high end of this, successful value enhancement programs have led to huge savings. Thai-based PET leader Indorama Ventures’ “Project Olympus” delivered over US$600 million in cost savings. Similarly, Borouge, a JV between ADNOC and Austria’s Borealis, also delivered US$607 million in positive EBITDA as part of its Value Enhancement Program.

On the M&A front, transactions that match feedstock with the market, potentially from the Middle East into Asia, are likely. The recent acquisition by Thai-Indonesian Chandra Asri, in JV with Glencore of Shell’s refinery in Singapore is one example of intra-regional investment that could give Indonesia’s only naphtha cracker better access to feedstock via Singapore. According to Thomas Luedi, leading Asia chemicals and commercial excellence practices for Bain and Company, standalone (or non-integrated) crackers are the most vulnerable in the current environment and will continue to face challenges, whereas crackers integrated back to refineries have a better cost position. That incentivizes non-integrated crackers to look for feedstock options.

With naphtha prices on a downward trend, futures trading at about US$660/ton, and contract net transaction prices at about half that range, Southeast Asian petrochemical producers should see marginal improvements in the near term. However, the long-term view is uncertain with overcapacities in the olefin space threatening the prices of petrochemicals and expectations that oil and refining could potentially play a bigger role in petrochemicals. A second wave of mainland Chinese naptha crackers is taking shape, writes Chemical Markets Analytics (Dow Jones company). This is primarily led by state-owned enterprises. The new supply could send the ethylene market into oversupply.

Between 1995 and 2020, the chemical industry grew more slowly (175%) than the world GDP (149%), according to the Information Technology and Innovation Foundation (ITIF), a think tank. The correlation between GDP and chemicals has historically been a close one, but this may no longer be the case, the energy transition pressurizing both the oil and gas and chemical sectors to prepare for a lower-carbon future. That makes demand uncertain, especially for countries relying heavily on exports to China, like Singapore and Thailand, whereas Indonesia and Vietnam remain busy with their under-supplied domestic sector. It will be interesting to see whether more petrochemical complexes in these two countries could make sense in light of capacity additions elsewhere.

One thing that Southeast Asian countries could learn from China is investing beyond quarterly performance. China has invested during “sickness and health,” driven not solely by profits, but by the longer-term prospects of job creation, stability, and advancing market positions when others were preoccupied with overheads or paused to mend the wounds of past and present challenges. Of course, few have the luxury of subsidies, scale, and integration with a humongous manufacturing sector that China grants, but there are still many spots to fill in specialty chemicals before China catches up to those too.

China is currently in a situation of “low-end surplus, high-end shortage,” which means it has excess or severe excess supply of up to 75% by 2025 in petrochemical products, but it still has to import 50% of its higher-end chemicals, as found by German newspaper CheManager International. With the capacity-demand ratio growing in basic chemicals like ethylene oxide or PTA forcing a reduction in Chinese utilization rates, in 2021 China issued the ”Market Access Negative List” to restrict new chemical projects in saturated areas like ethylene, p-xylene, and coal-to-olefins and coal-to-paraxylene projects, directing its focus on the higher-value markets, including synthetic materials, functional materials or electronic chemicals. China is the largest consumer of specialty chemicals in the world, but it could be a matter of time before the country starts tackling this gap.

In the meantime, the country that is bringing the most hope for petrochemical makers is India, whose demand for PE and PP is on an upward trend, according to S&P statistics. However, competition to serve this hungry sector will be cutthroat, and Southeast Asian companies do not have the upper hand on costs.

Ubolrat Wiwattanakul, leading Southeast Asia for Lummus Technology, leaves us with the concluding thought for this article: “People used to think in cycles before, but there are bigger things on the horizon now – conflicts, oil crises, shifting geopolitics – all overwriting supply-to-demand fundamentals. The Southeast Asian petrochemical industry has the fighting spirit to invest in its population. If the regional industry operates only in the low-cost arena, there is always going to be a new player producing cheaper.