IMAGE: Courtesy of Gold Fields

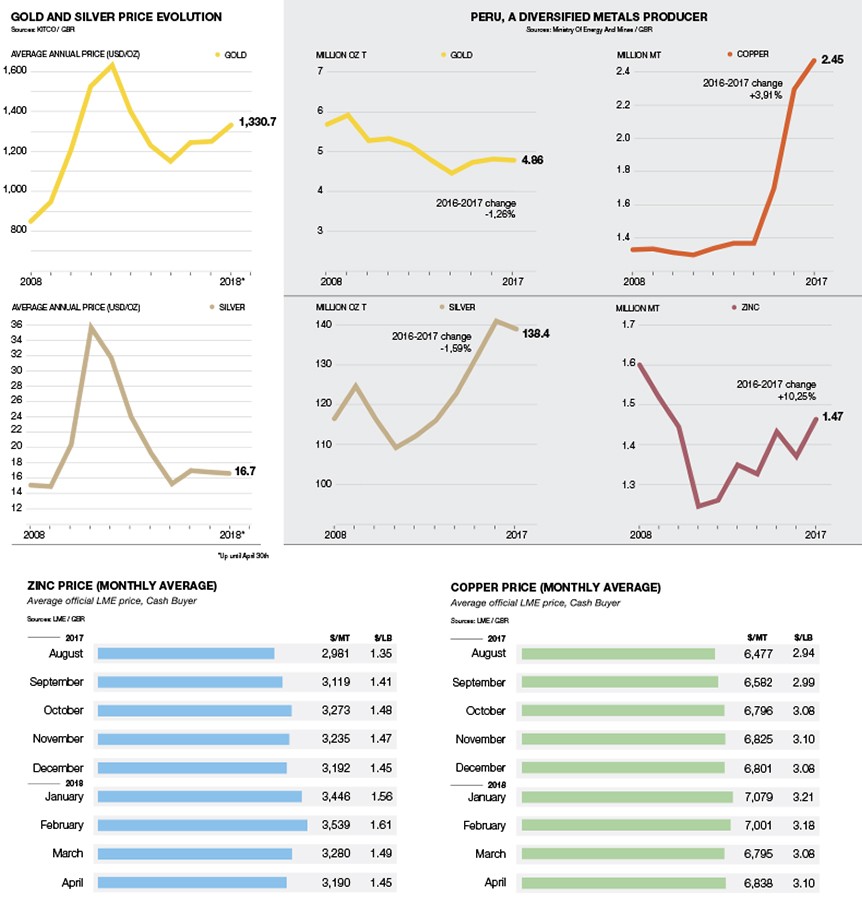

Peru maintains a key position in precious metals mining and development. In 2017, it remained the world’s sixth largest gold producer (and the largest in Latin America), while it was also the world’s second largest silver producer, only after Mexico.

Peru’s gold production remained relatively stable and only recorded a 1.2% decrease year-on-year. Total output reached 4.86 million troy ounces, with Yanacocha contributing 535,700 oz. This still places the operation, located in Cajamarca, as the country’s largest gold mine despite its continuous decline. The guidance for this year is around the half a million-ounce mark and, with the Quecher Main project, its life should be extended until 2027. Quecher Main, a US$250 million to US$300 million venture, will add new output from oxides starting next year, with expected production of 200,000 oz/y between 2020 and 2025.

Yanacocha is a joint venture between Newmont, that operates the mine, Buenaventura, and Sumitomo, that recently acquired a 5% stake. On top of its share of production at Yanacocha (43.65% of the total, or 233,400 oz), Buenaventura also had an additional attributable production of 383,200 ounces from the other gold mines it operates, namely Tambomayo, Orcopampa, La Zanja and Tantahuatay.

Víctor Gobitz, CEO of Buenaventura, anticipated higher production figures this year from Tambomayo, which reached commercial production last year, and at Coimolache, where the company is processing the oxide stockpiles acquired from neighboring Cerro Corona. He also provided more details about the three-year debottlenecking project at the company’s main underground mines: “In Orcopampa, the deeper side of the mine offers high grade but we have not developed a shaft, so with the ramp we are extracting less volumes at higher costs, including additional ventilation costs. In other mines, we are implementing better ventilation or dewatering solutions to extend the mine cycles. We also want to move our backfill around as slurry, with pumps, rather than having to use trucks and scoops.”

Gobitz explained that allocating funds to improve efficiency presents less technical risk and a quicker return on investment than developing a greenfield project. Having said that, Buenaventura also has some precious metals projects in the pipeline, including the San Gabriel gold project and the Yumpaq satellite silver deposit at Uchucchacua.

Beyond Newmont and Buenaventura, the other large gold producers include Barrick, that recorded 508,700 ounces between Lagunas Norte and Pierina; Tahoe Resources, that produced 275,000 oz at its La Arena and Shahuindo mines; and Gold Fields, that had production of 166,000 oz of gold at Cerro Corona, a medium-sized mine in Cajamarca that also provides important copper volumes (gold equivalent production is 314,000 oz).

Stretching mine-life

In 2017, Barrick’s Lagunas Norte produced 387,000 oz at an all-in sustaining cost (AISC) below US$500/oz, while there is an expected decline to between 230,000 and 270,000 oz this year, related to the depletion of the oxide ores. One of the main developments in 2018 is the building of a dry screener, while the company continues working on the refractory ore project (PMR in Spanish). Lagunas Norte has around 4 million ounces in reserves, most of which is sulfides.

According to the company’s executive director in Peru, Manuel Fumagalli, a transitional phase for mine-life extension would involve a mill and carbon-in-leach recovery circuit to process the medium-to-high carbonaceous oxide material in the stockpiles for a total output of 600,000 oz between 2021 and 2026. Then, the PMR project would require a flotation and autoclave process for the sulfides and, if approved, would produce 2.2 million ounces starting in 2026.

Meanwhile, Gold Fields has also pushed to add mine-life at its Cerro Corona mine, with a seven-year extension to this operation, now expected to be running until 2030. Luis Rivera, executive vice-president of Gold Fields for the Americas, explained: “Mining is like a credit card, it has an expiration date. At the beginning of 2017, Cerro Corona was scheduled to shut down in 2023. That meant that, from 2018, we would have had to start closure activities, reducing our footprint and our workforce. We made it an urgency to extend the mine life.”

Considering the space limitations Cerro Corona faces in Cajamarca, achieving this took its share of engineering and creativity. Alberto Cárdenas, vice-president of operations at Gold Fields, commented: “The beauty of the solution is that we are not extending the superficial footprint. We are challenging the density of the tailings to accommodate more volume within the same facility. Also, at the end of the day, the pit is also an asset, so we are looking at placing some tailings within the pit after the operation.”

Also in Cajamarca, Tahoe Resources continues to ramp up its operation at Shahuindo, where it is commissioning a crushing and agglomeration (C&A) plant to improve recoveries from the fines of the ore body (production of 79,000 ounces in 2017 came from run-of-mine ore). Once the plant is commissioned, Tahoe will embark on the expansion of Shahuindo from 12,000 mt/d to 36,000 mt/d. “Our other Shahuindo projects, such as resourcing water, constructing pads and building a transmission line, are also key. Near-mine and satellite geological deposits in the north corridor of Shahuindo provide us potential targets to extend and maximize value at this operation,” said Phil Dalke, until recently vice-president and managing director of Tahoe Peru.

Peruvian companies account for significant gold production as well. These include Poderosa (254,000 oz/y), Horizonte (253,000 oz/y), and Hochschild Mining, traditionally a primary silver producer, that has been increasingly leaning towards gold production with the impulse of the Inmaculada mine. Hochschild produced 203,600 oz of gold in Peru last year, and 165,000 of those ounces came from this flagship asset.

With respect to Poderosa, the company is currently expanding its processing capacity from the combined 1,400 mt/d in between its Marañón and Santa María plants, to 1,600 mt/d by the end of this year. One of the main items of the expansion in terms of the capex are the tailings dams, explained Marcelo Santillana, general manager of Poderosa: “With the investments in the Livias and Hualanga facilities, the tailings dams will now have a life of 22 years. Moreover, we filter the tailings, so we do not deal with pulp anymore.”

Poderosa expects to produce 270,000 ounces of gold this year and continues to look at formulas to optimize production and extend mine-life.

Elsewhere in La Libertad, Corporación del Centro (CDC Gold) is advancing the El Toro project, an epithermal gold deposit hosting around 1 million ounces, that is being developed as an open pit operation with heap leaching and a carbon-in-column plant. Initial production is estimated at 100,000 oz/y. Construction is already under way and mining operations should start before the end of the year. Jaime Polar, general manager of CDC Gold, gave more details: “Our stripping ratio is quite good, just 2:1 according to our mine plan, and we also have favorable hydrogeological studies that indicate that we will not have to dewater the pit. In its first phase, the capital investment to put El Toro into production amounts to around US$150 million.”

Silver

Silver production in Peru also decreased by 1.6%, totaling 138.4 million ounces. Buenaventura is the country’s largest silver producer with 23.3 million ounces in 2017, a figure that does not include the additional 4 million ounces coming from El Brocal, another company that it controls. The other main silver producers in the country are Antamina, with 20.8 million oz/y; Volcan, with 15.9 million oz/y; and Hochschild Mining, with 15.9 million oz/y.

The latter company had production costs of around US$12.5/oz silver equivalent last year, and those should increase slightly in 2018 to between US$13/oz and US$13.4/oz according to the corporate guidance. Part of this cost increase is the US$30-million investment in the Pablo development at the Pallancata mine in Peru. “In 2017, Pallancata was working at 1,400 metric tons per day (mt/d). Through incremental expansions, we will reach 2,800 mt/d by Q3 2018, and production will stabilize at that rate,” explained Ignacio Bustamante, CEO of Hochschild Mining.

A new player in Peru is Great Panther Silver, a company with operations in Mexico, that is working to reopen the Coricancha mine in Peru after acquiring the asset from Nyrstar. The company has recently published a preliminary economic assessment (PEA) that anticipates future production from Coricancha will be 3.1 million oz/y, an internal rate of return (IRR) of 81% and a relatively low capex to get the mine restarted at US$8.8 million. The initial mine-life of four years comprises 28% of Coricancha’s resource statement. Great Panther is now embarking on a 6,000 mt bulk sample program to test the mining method, recoveries and dilution rates. Great Panther’s objective is to have the mine fully up and running by the end of 2019.

“Our study anticipates using a combination of resue mining and captive cut and fill, which is a mechanized method with very small equipment,” said James Bannantine, president and CEO of Great Panther Silver. “Nyrstar suffered from dilution, so our main focus is going to be dilution-control, which means lower volume and higher selectivity for narrow mining width, as well as having more mining faces,” he concluded.

Finally, Bear Creek Mining continues advancing at Corani, a very large silver deposit with significant base metal content. Potentially moving into construction over the next year, and with expected production of 12 million oz/y during the first six years of operation, Corani is one of those ‘company makers’ that do not come in production very often in the industry.

Of course, such a large project brings significant risk with it. Through recent engineering, the company has reduced the estimated capex of the project to a US$585-million figure, which is still high for a junior player transitioning to become a mining company. Anthony Hawkshaw, president and CEO of Bear Creek, said: “There are areas to save money and initial engineering observations have identified possible capex reductions.”

In May 2018, the company received its mine construction and water permits. Bear Creek will wait for a “compelling project financing structure” before taking a final construction decision.

IMAGE: Courtesy of Gold Fields

Peru maintains a key position in precious metals mining and development. In 2017, it remained the world’s sixth largest gold producer (and the largest in Latin America), while it was also the world’s second largest silver producer, only after Mexico.

Peru’s gold production remained relatively stable and only recorded a 1.2% decrease year-on-year. Total output reached 4.86 million troy ounces, with Yanacocha contributing 535,700 oz. This still places the operation, located in Cajamarca, as the country’s largest gold mine despite its continuous decline. The guidance for this year is around the half a million-ounce mark and, with the Quecher Main project, its life should be extended until 2027. Quecher Main, a US$250 million to US$300 million venture, will add new output from oxides starting next year, with expected production of 200,000 oz/y between 2020 and 2025.

Yanacocha is a joint venture between Newmont, that operates the mine, Buenaventura, and Sumitomo, that recently acquired a 5% stake. On top of its share of production at Yanacocha (43.65% of the total, or 233,400 oz), Buenaventura also had an additional attributable production of 383,200 ounces from the other gold mines it operates, namely Tambomayo, Orcopampa, La Zanja and Tantahuatay.

Víctor Gobitz, CEO of Buenaventura, anticipated higher production figures this year from Tambomayo, which reached commercial production last year, and at Coimolache, where the company is processing the oxide stockpiles acquired from neighboring Cerro Corona. He also provided more details about the three-year debottlenecking project at the company’s main underground mines: “In Orcopampa, the deeper side of the mine offers high grade but we have not developed a shaft, so with the ramp we are extracting less volumes at higher costs, including additional ventilation costs. In other mines, we are implementing better ventilation or dewatering solutions to extend the mine cycles. We also want to move our backfill around as slurry, with pumps, rather than having to use trucks and scoops.”

Gobitz explained that allocating funds to improve efficiency presents less technical risk and a quicker return on investment than developing a greenfield project. Having said that, Buenaventura also has some precious metals projects in the pipeline, including the San Gabriel gold project and the Yumpaq satellite silver deposit at Uchucchacua.

Beyond Newmont and Buenaventura, the other large gold producers include Barrick, that recorded 508,700 ounces between Lagunas Norte and Pierina; Tahoe Resources, that produced 275,000 oz at its La Arena and Shahuindo mines; and Gold Fields, that had production of 166,000 oz of gold at Cerro Corona, a medium-sized mine in Cajamarca that also provides important copper volumes (gold equivalent production is 314,000 oz).

Stretching mine-life

In 2017, Barrick’s Lagunas Norte produced 387,000 oz at an all-in sustaining cost (AISC) below US$500/oz, while there is an expected decline to between 230,000 and 270,000 oz this year, related to the depletion of the oxide ores. One of the main developments in 2018 is the building of a dry screener, while the company continues working on the refractory ore project (PMR in Spanish). Lagunas Norte has around 4 million ounces in reserves, most of which is sulfides.

According to the company’s executive director in Peru, Manuel Fumagalli, a transitional phase for mine-life extension would involve a mill and carbon-in-leach recovery circuit to process the medium-to-high carbonaceous oxide material in the stockpiles for a total output of 600,000 oz between 2021 and 2026. Then, the PMR project would require a flotation and autoclave process for the sulfides and, if approved, would produce 2.2 million ounces starting in 2026.

Meanwhile, Gold Fields has also pushed to add mine-life at its Cerro Corona mine, with a seven-year extension to this operation, now expected to be running until 2030. Luis Rivera, executive vice-president of Gold Fields for the Americas, explained: “Mining is like a credit card, it has an expiration date. At the beginning of 2017, Cerro Corona was scheduled to shut down in 2023. That meant that, from 2018, we would have had to start closure activities, reducing our footprint and our workforce. We made it an urgency to extend the mine life.”

Considering the space limitations Cerro Corona faces in Cajamarca, achieving this took its share of engineering and creativity. Alberto Cárdenas, vice-president of operations at Gold Fields, commented: “The beauty of the solution is that we are not extending the superficial footprint. We are challenging the density of the tailings to accommodate more volume within the same facility. Also, at the end of the day, the pit is also an asset, so we are looking at placing some tailings within the pit after the operation.”

Also in Cajamarca, Tahoe Resources continues to ramp up its operation at Shahuindo, where it is commissioning a crushing and agglomeration (C&A) plant to improve recoveries from the fines of the ore body (production of 79,000 ounces in 2017 came from run-of-mine ore). Once the plant is commissioned, Tahoe will embark on the expansion of Shahuindo from 12,000 mt/d to 36,000 mt/d. “Our other Shahuindo projects, such as resourcing water, constructing pads and building a transmission line, are also key. Near-mine and satellite geological deposits in the north corridor of Shahuindo provide us potential targets to extend and maximize value at this operation,” said Phil Dalke, until recently vice-president and managing director of Tahoe Peru.

Peruvian companies account for significant gold production as well. These include Poderosa (254,000 oz/y), Horizonte (253,000 oz/y), and Hochschild Mining, traditionally a primary silver producer, that has been increasingly leaning towards gold production with the impulse of the Inmaculada mine. Hochschild produced 203,600 oz of gold in Peru last year, and 165,000 of those ounces came from this flagship asset.

With respect to Poderosa, the company is currently expanding its processing capacity from the combined 1,400 mt/d in between its Marañón and Santa María plants, to 1,600 mt/d by the end of this year. One of the main items of the expansion in terms of the capex are the tailings dams, explained Marcelo Santillana, general manager of Poderosa: “With the investments in the Livias and Hualanga facilities, the tailings dams will now have a life of 22 years. Moreover, we filter the tailings, so we do not deal with pulp anymore.”

Poderosa expects to produce 270,000 ounces of gold this year and continues to look at formulas to optimize production and extend mine-life.

Elsewhere in La Libertad, Corporación del Centro (CDC Gold) is advancing the El Toro project, an epithermal gold deposit hosting around 1 million ounces, that is being developed as an open pit operation with heap leaching and a carbon-in-column plant. Initial production is estimated at 100,000 oz/y. Construction is already under way and mining operations should start before the end of the year. Jaime Polar, general manager of CDC Gold, gave more details: “Our stripping ratio is quite good, just 2:1 according to our mine plan, and we also have favorable hydrogeological studies that indicate that we will not have to dewater the pit. In its first phase, the capital investment to put El Toro into production amounts to around US$150 million.”

Silver

Silver production in Peru also decreased by 1.6%, totaling 138.4 million ounces. Buenaventura is the country’s largest silver producer with 23.3 million ounces in 2017, a figure that does not include the additional 4 million ounces coming from El Brocal, another company that it controls. The other main silver producers in the country are Antamina, with 20.8 million oz/y; Volcan, with 15.9 million oz/y; and Hochschild Mining, with 15.9 million oz/y.

The latter company had production costs of around US$12.5/oz silver equivalent last year, and those should increase slightly in 2018 to between US$13/oz and US$13.4/oz according to the corporate guidance. Part of this cost increase is the US$30-million investment in the Pablo development at the Pallancata mine in Peru. “In 2017, Pallancata was working at 1,400 metric tons per day (mt/d). Through incremental expansions, we will reach 2,800 mt/d by Q3 2018, and production will stabilize at that rate,” explained Ignacio Bustamante, CEO of Hochschild Mining.

A new player in Peru is Great Panther Silver, a company with operations in Mexico, that is working to reopen the Coricancha mine in Peru after acquiring the asset from Nyrstar. The company has recently published a preliminary economic assessment (PEA) that anticipates future production from Coricancha will be 3.1 million oz/y, an internal rate of return (IRR) of 81% and a relatively low capex to get the mine restarted at US$8.8 million. The initial mine-life of four years comprises 28% of Coricancha’s resource statement. Great Panther is now embarking on a 6,000 mt bulk sample program to test the mining method, recoveries and dilution rates. Great Panther’s objective is to have the mine fully up and running by the end of 2019.

“Our study anticipates using a combination of resue mining and captive cut and fill, which is a mechanized method with very small equipment,” said James Bannantine, president and CEO of Great Panther Silver. “Nyrstar suffered from dilution, so our main focus is going to be dilution-control, which means lower volume and higher selectivity for narrow mining width, as well as having more mining faces,” he concluded.

Finally, Bear Creek Mining continues advancing at Corani, a very large silver deposit with significant base metal content. Potentially moving into construction over the next year, and with expected production of 12 million oz/y during the first six years of operation, Corani is one of those ‘company makers’ that do not come in production very often in the industry.

Of course, such a large project brings significant risk with it. Through recent engineering, the company has reduced the estimated capex of the project to a US$585-million figure, which is still high for a junior player transitioning to become a mining company. Anthony Hawkshaw, president and CEO of Bear Creek, said: “There are areas to save money and initial engineering observations have identified possible capex reductions.”

In May 2018, the company received its mine construction and water permits. Bear Creek will wait for a “compelling project financing structure” before taking a final construction decision.