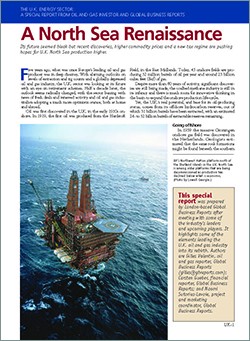

Five years ago, what was once Europe’s leading oil and gas producer was in deep disarray. With alarming outlooks on levels of extraction and rig counts and a globally depressed oil and gas industry, the U.K. sector was looking at its future with an eye on retirement schemes. Half a decade later, the outlook seems radically changed, with the sector buzzing with news of fresh deals and renewed activity and oil and gas industrialists adopting a much more optimistic stance, both at home and abroad.

Today, 45 onshore fields are producing 32 million barrels of oil per year and around 23 billion cubic feet (Bcf) of gas. Despite more than 80 years of activity, significant discoveries are still being made, the coalbed-methane industry is still in its infancy and there is much room for innovative thinking in the basin to expand the onshore production life-cycle. Yet, the U.K.’s real potential, and base for its oil-producing status, comes from its offshore hydrocarbon reserves, out of which 31 billion barrels have been extracted, with an estimated 24 to 32 billion barrels of extractable reserves remaining.

Five years ago, what was once Europe’s leading oil and gas producer was in deep disarray. With alarming outlooks on levels of extraction and rig counts and a globally depressed oil and gas industry, the U.K. sector was looking at its future with an eye on retirement schemes. Half a decade later, the outlook seems radically changed, with the sector buzzing with news of fresh deals and renewed activity and oil and gas industrialists adopting a much more optimistic stance, both at home and abroad.

Today, 45 onshore fields are producing 32 million barrels of oil per year and around 23 billion cubic feet (Bcf) of gas. Despite more than 80 years of activity, significant discoveries are still being made, the coalbed-methane industry is still in its infancy and there is much room for innovative thinking in the basin to expand the onshore production life-cycle. Yet, the U.K.’s real potential, and base for its oil-producing status, comes from its offshore hydrocarbon reserves, out of which 31 billion barrels have been extracted, with an estimated 24 to 32 billion barrels of extractable reserves remaining.