Image by Tyler Prahm at Unsplash

Some of the financing woes Ontario’s juniors felt in 2023 continued into 2024, with many of them reporting that the equity markets are not favorable despite record metal and mineral prices. There are a myriad of reasons for this, with a federal government clampdown on Chinese foreign investment, uncertainty from US presidential elections and a sheepish retail investor base being just some of the factors behind Ontario juniors’ financing woes.

The issue is particularly pronounced with critical minerals-focused companies, many of which have not enjoyed the favorable prices currently experienced by precious metals companies. In a recent survey by the Canadian Climate Institute, 87% of respondents agreed that the current level of investments is “insufficient” to grow Canada’s critical minerals value chain. Despite government efforts to spur investments through grants and subsidies, the lack of private capital entering Canada’s mining sector is making it difficult to close the financing gap. “Unfortunately, over the last few years we have not seen as much capital flow into institutional investor funds in Canada focused on metals and mining as we used to, so Canada’s relevance as a source of institutional investor dollars in this space has been

Of the institutional investors that still have an appetite for junior exploration stocks, ETFs are becoming the preferred option. As investors shy away from the risk of picking individual stocks, many juniors not included in certain ETFs miss out on crucial funding. “The challenge lies in how many institutional investors have shifted to directly investing in commodities, favoring ETFs and using quantitative management over individual stock picking,” said Trevor Turnbull, managing director – global mining & metals, banking, National Bank Financial.

For the smaller juniors that do not meet the requirements to be included in dominant ETFs, like the VanEck Junior Gold Miners ETF (GDXJ), equity financing is made all the more difficult. “Among intermediate and junior players, inclusion in the GDXJ ETF remains a key differentiator. However, the absence of specialty funds focused on creating value beyond the GDXJ limits growth opportunities for small-cap juniors. Nevertheless, a market shift could emerge to exploit the distortion between intrinsic and market value for these companies,” said Alejandro Hoyos, VP, metals & mining investment banking, Stifel Canada.

While many of Ontario’s gold majors have seen their share prices rise steadily to reflect the rising price of the gold they are producing, many juniors feel they are unfairly undervalued and investors eyes are elsewhere. Although the GDXJ has generally lagged behind the rising gold price over the past year, there have been some signs of hope: “Just before the US elections, the GDXJ started to cross the line of the GDX, narrowing the gap with the GDX and suggesting that there was interest coming back into that space. However, challenges persist in Canada, particularly regarding Indigenous community issues, which continue to delay project advancement. Governments must address this challenge as quickly as possible,” said Rob McEwen, chairman and chief owner, McEwen Mining.

Uncertainty concerning project timelines has undoubtably pushed some investors away from Ontario’s junior mining space. Additionally, in the case of critical minerals, many feel that government support through initiatives like the CMIF have focused too much on downstream battery plants and surrounding infrastructure, rather than putting money in the ground for actual exploration. “The challenge is that the funds earmarked by the government and the investment of various interest groups tend to be focused on the pieces of the mining industry that are not extractive. People are hesitant to invest in the extraction process and would rather be involved in building infrastructure, so there is not as much support for the upstream sector,” said Michael Pickersgill, head of mining and metals, Torys LLP.

Ontario’s mining sector continues to struggle to tempt the new profiles of institutional investors with a sufficient appetite for riskier early-stage exploration plays. “Pension funds are not investing in exploration, so resource funds continue to be the primary capital source, despite weak inflows. There has not been a noticeable trend of new investor types, and sovereign wealth funds show only sporadic interest. Private equity is more active now compared to 15-20 years ago, but its impact on the sector remains limited,” said Craig Stanley, director – precious metals, Raymond James.

Toronto’s financial institutions are having to provide new forms of financing to fill the gap, especially for juniors who feel their trading multiples are too low for traditional equity raising. “We are increasingly being asked to help by lending or through creative solutions like At-The-Market financings (ATMs), which allow companies to raise funds steadily throughout the year without impacting share prices as traditional deals might. Prepaids, where some future production is sold upfront, have also gained in popularity,” said Turnbull.

The inability of Canada to attract more generalist investors to its mining sector has a knock-on effect on resource funds, which typically have technical backgrounds and are more inclined to look at higher-risk exploration opportunities. “Liquidity, which is typically driven by generalist retail investors, can suffer when market attention is attracted to other sectors, for example technology,” said Stefan Ioannou, base metals analyst, institutional equity research, Cormark Securities.

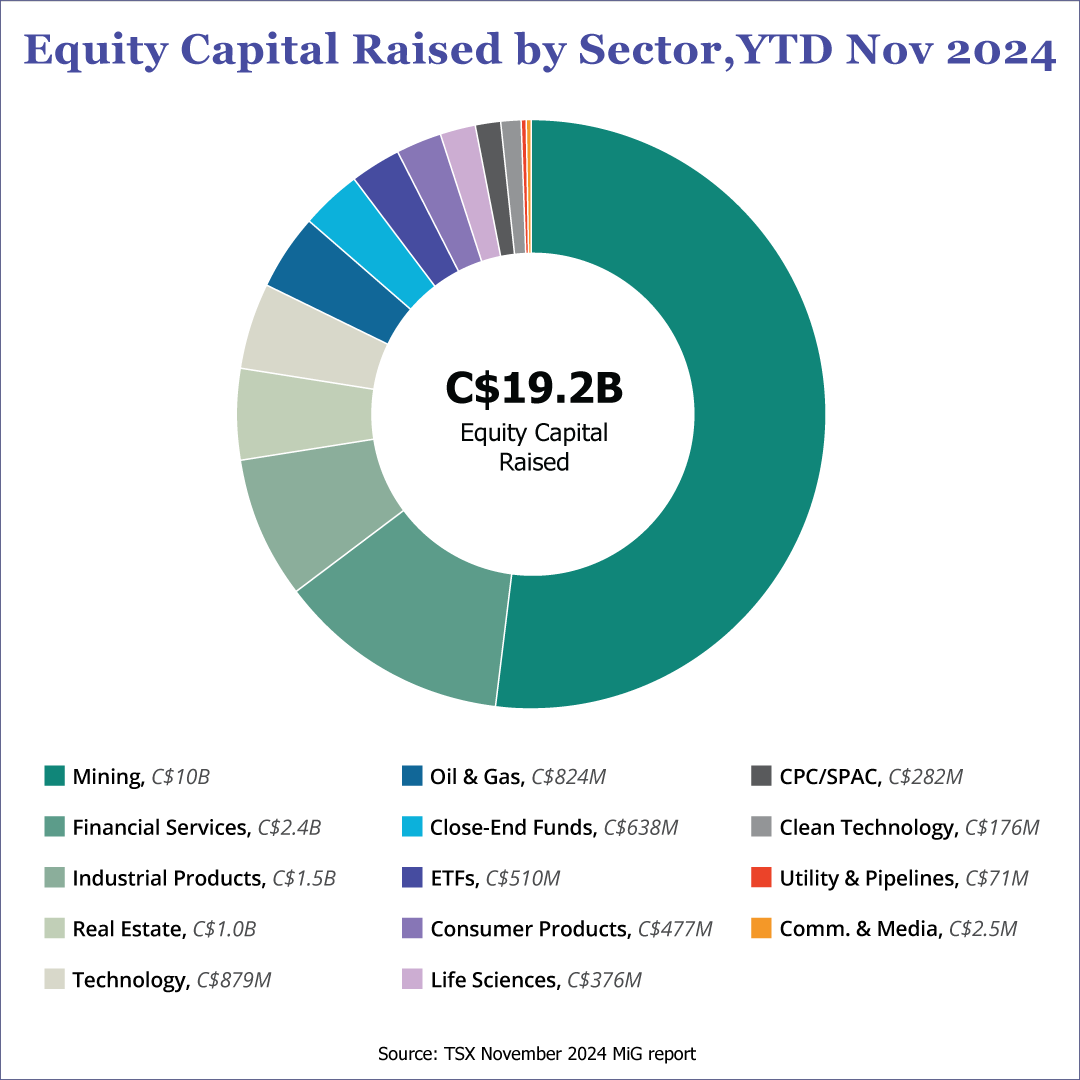

There are signs of improvement, however, with the mining and exploration companies listed on the TSX and TSXV collectively raising C$6.8 billion in equity capital in H1 2024, a 62% gain compared to the same period in 2023, and First Quantum closing a C$1 billion equity bought deal, the largest in Canada’s history. “The pandemic, geopolitical tensions, and a high inflationary environment had a great impact on the global mining sector and the financing market has not yet returned to the levels we saw in 2021, but the upward trend we have experienced in 2024 thus far has been encouraging, and the interest rate cuts by Canada, Europe and now the US, as well as increasing commodity prices, have given the mining sector reasons to again be optimistic,” said Dean McPherson, head, business development – global mining, Toronto Stock Exchange and TSX Venture Exchange.

Investment Canada Act

A recent overhaul to the Investment Canada Act (ICA) has been a hot topic of conversation on Bay Street. The changes represent the most significant update to the national security provisions of the ICA since they were first adopted in 2009, and all point towards increased scrutiny of foreign investment in Canadian critical minerals projects – particularly from China. The changes have seen new surtaxes and tariffs on Chinese imports and it is likely that more cases of Chinese investments into Canadian mining companies will become unfeasible or outright refused, as evidenced by Solaris Resources recently scrapping its plan to sell a minority stake to Zinjin Mining Group. “Companies that were previously relying on foreign investments to raise capital now face challenges. The problem is further compounded when a significant portion of production and processing, especially for critical minerals, is happening in countries like China, and therefore some of the natural investors are foreign investors seeking feedstock,” said Denis Frawley, partner, Momentum Law LLP.

The controversial changes have been met by resistance from small-cap Canadian explorers to the CEO of the TMX group. The matter is further complicated by the fact that many mining companies are headquartered in Canada and listed on Canadian exchanges, but have projects abroad. “All Canadians would agree with the intent to protect our national interest in the critical minerals supply chain. The execution however has only served to create confusion with its lack of clarity and consistency, with many of the cases involving projects which are located outside of Canada. We have already seen companies taking steps to protect themselves from the Canadian government by redomiciling, while keeping their TSX/V listing,” continued McPherson.

Beyond the immediate financing challenges caused by Canada’s hawkish stance towards China, the ICA changes also risk hampering Canadian prospectors’ and miners’ chances at developing projects abroad in the long term. “Canada is a global mining leader and is setting a benchmark for how other countries conduct themselves in the mining space. Therefore, the government must not make arbitrary decisions about who can and cannot invest in mining operations, as we run the risk that it will get turned around on us. Many of Canada’s leading mining companies rely on foreign countries being receptive to them operating in their jurisdictions. Canada should set a positive tone in terms of international mining investment,” said Paul Brink, president and CEO, Franco-Nevada Corporation.

Although the Canadian government is turning its back on China, it has looked to build stronger relationships with other nations to fill the gap, at least in the critical minerals space. For Green Technology Metals (GT1), an Australian company looking to become Ontario’s first lithium producer, this has opened new avenues for partnerships and financing, evidenced by its investment from Korean battery maker EcoPro: “Canada’s restrictive stance on Chinese financing has made things easier for us. Canada has been actively strengthening relationships with South Korea and Japan, particularly in critical minerals and infrastructure development. During my recent trip to Korea, I met with the Canadian Trade Commissioner, who is helping facilitate partnerships between Korean investors and Canadian projects,” shared GT1’s managing director Cameron Henry.

Similarly, Frontier Lithium entered a JV with Japanese carmaker Mitsubishi and Canada Nickel received a significant investment from Korean conglomerate Samsung SDI. “The Canadian government is actively supporting these relationships under objectives of achieving carbon neutrality and economic security, and intending to strengthen coordination between Canada and Japan to build sustainable and reliable global battery supply chains from upstream to downstream. While Chinese partnerships have historically been significant, we are confident that growing support from other global leaders will strengthen the foundation for a secure and sustainable supply chain in Canada and the US,” said Trevor Walker, president and CEO, Frontier Lithium.

However, investment from Korean and Japanese multinationals into Ontario’s junior space appear to be limited to select commodities used in EV and battery manufacturing. For gold-focused juniors, who are far more numerous in Ontario, such partnerships are unlikely to be an option.

Image by Tyler Prahm at Unsplash

Some of the financing woes Ontario’s juniors felt in 2023 continued into 2024, with many of them reporting that the equity markets are not favorable despite record metal and mineral prices. There are a myriad of reasons for this, with a federal government clampdown on Chinese foreign investment, uncertainty from US presidential elections and a sheepish retail investor base being just some of the factors behind Ontario juniors’ financing woes.

The issue is particularly pronounced with critical minerals-focused companies, many of which have not enjoyed the favorable prices currently experienced by precious metals companies. In a recent survey by the Canadian Climate Institute, 87% of respondents agreed that the current level of investments is “insufficient” to grow Canada’s critical minerals value chain. Despite government efforts to spur investments through grants and subsidies, the lack of private capital entering Canada’s mining sector is making it difficult to close the financing gap. “Unfortunately, over the last few years we have not seen as much capital flow into institutional investor funds in Canada focused on metals and mining as we used to, so Canada’s relevance as a source of institutional investor dollars in this space has been

Of the institutional investors that still have an appetite for junior exploration stocks, ETFs are becoming the preferred option. As investors shy away from the risk of picking individual stocks, many juniors not included in certain ETFs miss out on crucial funding. “The challenge lies in how many institutional investors have shifted to directly investing in commodities, favoring ETFs and using quantitative management over individual stock picking,” said Trevor Turnbull, managing director – global mining & metals, banking, National Bank Financial.

For the smaller juniors that do not meet the requirements to be included in dominant ETFs, like the VanEck Junior Gold Miners ETF (GDXJ), equity financing is made all the more difficult. “Among intermediate and junior players, inclusion in the GDXJ ETF remains a key differentiator. However, the absence of specialty funds focused on creating value beyond the GDXJ limits growth opportunities for small-cap juniors. Nevertheless, a market shift could emerge to exploit the distortion between intrinsic and market value for these companies,” said Alejandro Hoyos, VP, metals & mining investment banking, Stifel Canada.

While many of Ontario’s gold majors have seen their share prices rise steadily to reflect the rising price of the gold they are producing, many juniors feel they are unfairly undervalued and investors eyes are elsewhere. Although the GDXJ has generally lagged behind the rising gold price over the past year, there have been some signs of hope: “Just before the US elections, the GDXJ started to cross the line of the GDX, narrowing the gap with the GDX and suggesting that there was interest coming back into that space. However, challenges persist in Canada, particularly regarding Indigenous community issues, which continue to delay project advancement. Governments must address this challenge as quickly as possible,” said Rob McEwen, chairman and chief owner, McEwen Mining.

Uncertainty concerning project timelines has undoubtably pushed some investors away from Ontario’s junior mining space. Additionally, in the case of critical minerals, many feel that government support through initiatives like the CMIF have focused too much on downstream battery plants and surrounding infrastructure, rather than putting money in the ground for actual exploration. “The challenge is that the funds earmarked by the government and the investment of various interest groups tend to be focused on the pieces of the mining industry that are not extractive. People are hesitant to invest in the extraction process and would rather be involved in building infrastructure, so there is not as much support for the upstream sector,” said Michael Pickersgill, head of mining and metals, Torys LLP.

Ontario’s mining sector continues to struggle to tempt the new profiles of institutional investors with a sufficient appetite for riskier early-stage exploration plays. “Pension funds are not investing in exploration, so resource funds continue to be the primary capital source, despite weak inflows. There has not been a noticeable trend of new investor types, and sovereign wealth funds show only sporadic interest. Private equity is more active now compared to 15-20 years ago, but its impact on the sector remains limited,” said Craig Stanley, director – precious metals, Raymond James.

Toronto’s financial institutions are having to provide new forms of financing to fill the gap, especially for juniors who feel their trading multiples are too low for traditional equity raising. “We are increasingly being asked to help by lending or through creative solutions like At-The-Market financings (ATMs), which allow companies to raise funds steadily throughout the year without impacting share prices as traditional deals might. Prepaids, where some future production is sold upfront, have also gained in popularity,” said Turnbull.

The inability of Canada to attract more generalist investors to its mining sector has a knock-on effect on resource funds, which typically have technical backgrounds and are more inclined to look at higher-risk exploration opportunities. “Liquidity, which is typically driven by generalist retail investors, can suffer when market attention is attracted to other sectors, for example technology,” said Stefan Ioannou, base metals analyst, institutional equity research, Cormark Securities.

There are signs of improvement, however, with the mining and exploration companies listed on the TSX and TSXV collectively raising C$6.8 billion in equity capital in H1 2024, a 62% gain compared to the same period in 2023, and First Quantum closing a C$1 billion equity bought deal, the largest in Canada’s history. “The pandemic, geopolitical tensions, and a high inflationary environment had a great impact on the global mining sector and the financing market has not yet returned to the levels we saw in 2021, but the upward trend we have experienced in 2024 thus far has been encouraging, and the interest rate cuts by Canada, Europe and now the US, as well as increasing commodity prices, have given the mining sector reasons to again be optimistic,” said Dean McPherson, head, business development – global mining, Toronto Stock Exchange and TSX Venture Exchange.

Investment Canada Act

A recent overhaul to the Investment Canada Act (ICA) has been a hot topic of conversation on Bay Street. The changes represent the most significant update to the national security provisions of the ICA since they were first adopted in 2009, and all point towards increased scrutiny of foreign investment in Canadian critical minerals projects – particularly from China. The changes have seen new surtaxes and tariffs on Chinese imports and it is likely that more cases of Chinese investments into Canadian mining companies will become unfeasible or outright refused, as evidenced by Solaris Resources recently scrapping its plan to sell a minority stake to Zinjin Mining Group. “Companies that were previously relying on foreign investments to raise capital now face challenges. The problem is further compounded when a significant portion of production and processing, especially for critical minerals, is happening in countries like China, and therefore some of the natural investors are foreign investors seeking feedstock,” said Denis Frawley, partner, Momentum Law LLP.

The controversial changes have been met by resistance from small-cap Canadian explorers to the CEO of the TMX group. The matter is further complicated by the fact that many mining companies are headquartered in Canada and listed on Canadian exchanges, but have projects abroad. “All Canadians would agree with the intent to protect our national interest in the critical minerals supply chain. The execution however has only served to create confusion with its lack of clarity and consistency, with many of the cases involving projects which are located outside of Canada. We have already seen companies taking steps to protect themselves from the Canadian government by redomiciling, while keeping their TSX/V listing,” continued McPherson.

Beyond the immediate financing challenges caused by Canada’s hawkish stance towards China, the ICA changes also risk hampering Canadian prospectors’ and miners’ chances at developing projects abroad in the long term. “Canada is a global mining leader and is setting a benchmark for how other countries conduct themselves in the mining space. Therefore, the government must not make arbitrary decisions about who can and cannot invest in mining operations, as we run the risk that it will get turned around on us. Many of Canada’s leading mining companies rely on foreign countries being receptive to them operating in their jurisdictions. Canada should set a positive tone in terms of international mining investment,” said Paul Brink, president and CEO, Franco-Nevada Corporation.

Although the Canadian government is turning its back on China, it has looked to build stronger relationships with other nations to fill the gap, at least in the critical minerals space. For Green Technology Metals (GT1), an Australian company looking to become Ontario’s first lithium producer, this has opened new avenues for partnerships and financing, evidenced by its investment from Korean battery maker EcoPro: “Canada’s restrictive stance on Chinese financing has made things easier for us. Canada has been actively strengthening relationships with South Korea and Japan, particularly in critical minerals and infrastructure development. During my recent trip to Korea, I met with the Canadian Trade Commissioner, who is helping facilitate partnerships between Korean investors and Canadian projects,” shared GT1’s managing director Cameron Henry.

Similarly, Frontier Lithium entered a JV with Japanese carmaker Mitsubishi and Canada Nickel received a significant investment from Korean conglomerate Samsung SDI. “The Canadian government is actively supporting these relationships under objectives of achieving carbon neutrality and economic security, and intending to strengthen coordination between Canada and Japan to build sustainable and reliable global battery supply chains from upstream to downstream. While Chinese partnerships have historically been significant, we are confident that growing support from other global leaders will strengthen the foundation for a secure and sustainable supply chain in Canada and the US,” said Trevor Walker, president and CEO, Frontier Lithium.

However, investment from Korean and Japanese multinationals into Ontario’s junior space appear to be limited to select commodities used in EV and battery manufacturing. For gold-focused juniors, who are far more numerous in Ontario, such partnerships are unlikely to be an option.