Image courtesy of Platform Petroleum

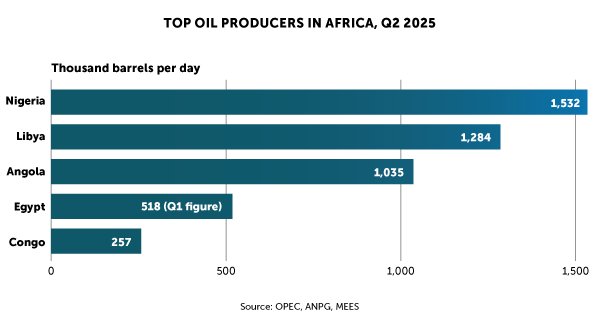

2025 is becoming a transformational year for the oil and gas industry in Sub-Saharan Africa as significant changes, transactions and policies are at play across the continent, both in mature and greenfield energy jurisdictions. Though the importance of oil and gas production in Africa is well known, it is important to point out that, per International Energy Association (IEA), crude oil production in Africa declined 13% between 2000-2022, pointing to a trend replicated in mature oil markets around the world, beset by natural production declines, but also reflecting some of the specifically African challenges of security and political instability that have also contributed to this decline, from Nigeria to Libya and other jurisdictions.

A similar scenario has played out with Africa’s midstream. The IEA data points to an even sharper drop for total oil products refined in Africa, with a 23% decline between 2000-2022. The significant difference is that whilst Africa accounted for 7% of global crude production in 2022, it only accounted for 2% of oil product refinement globally, which highlights just how much space there is for Africa’s mid and downstream sectors to grow, along with a rejigged upstream industry that can support this in-continent, homegrown development and beneficiation.

With an eye to the complementary and essential nature of upstream, midstream, and downstream activity and innovation to African prosperity and development, GBR has spent three months interviewing C-level executives in some of the most emblematic African hydrocarbon production and exploration countries, including Nigeria, Angola, Namibia, Ghana, Côte d’Ivoire and Senegal.

West Africa’s upstream is particularly awash with changes. In Nigeria, Indigenous companies have, in multi-billion-dollar transactions, taken ownership of onshore IOC assets in the Delta, which represents a historic moment for Nigeria and Sub-Saharan Africa’s oil and gas industry. In Senegal, Ghana and Côte d’Ivoire, upstream activity is accelerating. Eni launched Baleine Phase Two in Côte d’Ivoire, tripling oil production. Jean-Marc Kloss, SLB West Africa’s managing director, said: “One of the most significant projects in West Africa is Eni’s Baleine development in Côte d’Ivoire, which is Africa’s first net-zero upstream project. Beyond Côte d’Ivoire, SLB is involved in multiple high-profile projects across Ghana, Equatorial Guinea, Nigeria, Mauritania and Senegal.”

Despite the inherent challenges in West Africa, upstream development across the region unlocks opportunities for regional midstream and downstream development, strengthening energy security in an area with high levels of energy poverty. Mohammed Mijindadi, president of GE Vernova, Nigeria & managing director, Anglo-West & Francophone Africa, said: “Senegal, for example, having recently discovered gas reserves, is enhancing energy security and establishing itself as a regional energy hub.”

Natural gas projects are taking off across Sub-Saharan Africa. The resource is highly sought after in export markets and can foster domestic industrial development as a cheap, abundant source of energy. Mansur Mohammed, head of new business development Africa at Wood Mackenzie, said: “The rise of Floating LNG (FLNG) projects positions Sub-Saharan Africa as a global leader in this area. Cameroon, Congo, Senegal and Mauritania have FLNG projects, and others are developing theirs.”

Global markets dictate oil and gas developments in Sub-Saharan Africa as much as local developments. Charles Lowery, country manager and director of TEST Angola, said: “The foremost challenge remains the volatility of Brent crude prices. Short-term factors such as tariffs, global trade dynamics, the US political landscape, and Chinese demand influence market conditions. This volatility places pressure on investment flows, making capital allocation highly competitive. Paradoxically, the volume of tenders TEST Angola is bidding on is higher than ever. Despite the downturn in oil prices, this environment presents new opportunities for service providers, especially in mature markets like Angola where outsourcing services has become more cost-effective than in-house execution by the IOCs.”

Indeed, in South Africa, Angola and Namibia continue to attract attention. Angola’s upstream sector is maintaining production levels, and its regulatory entities have pushed for the onshore space to receive more attention. As natural production decline continues, further exploration work will be necessary, and small and mid-sized Independents will have to be drawn in to reinvigorate mature assets as IOCs transition to greener pastures. Those greener pastures in Africa find themselves further south, in Namibia. With a new president, the country is overhauling its oil and gas regulatory structure, as investors watch closely. Despite recent changes, discoveries continue to pick up the pace, and new players are entering the market, triggering an influx of international and African service providers into the country. The country’s coastal ports, at Walvis Bay and Lüderitz, are undergoing historical transformations, as will Namibia’s economy once the first oil is achieved.

Namibia’s financial establishment is readily adapting to the new oil & gas paradigm, but the deep need for both capital and time in long-term energy projects still presents a challenge. Rachel Mushabati, Senior Associate Attorney and Country Head: Namibia at CLG said “The local financing landscape is still unprepared for large-scale energy projects. Most of the financing still comes from international banks, export credit agencies, and private equity due to the sector’s high capital demands and associated risks.”

At the local level, the multi-faceted needs of a nascent oil & gas industry, including infrastructure development and human capital formation, are being confronted with financing constraints. Veronique Herman, CEO of Africa Provider Offshore Services (APOS), which provides training and certification services, said “Local companies need access to financial institutions that truly understand the specific challenges and opportunities of the oil and gas sector. We need banking partners who can evaluate projects holistically, respond quickly, and move beyond traditional models.”

Image courtesy of Platform Petroleum

2025 is becoming a transformational year for the oil and gas industry in Sub-Saharan Africa as significant changes, transactions and policies are at play across the continent, both in mature and greenfield energy jurisdictions. Though the importance of oil and gas production in Africa is well known, it is important to point out that, per International Energy Association (IEA), crude oil production in Africa declined 13% between 2000-2022, pointing to a trend replicated in mature oil markets around the world, beset by natural production declines, but also reflecting some of the specifically African challenges of security and political instability that have also contributed to this decline, from Nigeria to Libya and other jurisdictions.

A similar scenario has played out with Africa’s midstream. The IEA data points to an even sharper drop for total oil products refined in Africa, with a 23% decline between 2000-2022. The significant difference is that whilst Africa accounted for 7% of global crude production in 2022, it only accounted for 2% of oil product refinement globally, which highlights just how much space there is for Africa’s mid and downstream sectors to grow, along with a rejigged upstream industry that can support this in-continent, homegrown development and beneficiation.

With an eye to the complementary and essential nature of upstream, midstream, and downstream activity and innovation to African prosperity and development, GBR has spent three months interviewing C-level executives in some of the most emblematic African hydrocarbon production and exploration countries, including Nigeria, Angola, Namibia, Ghana, Côte d’Ivoire and Senegal.

West Africa’s upstream is particularly awash with changes. In Nigeria, Indigenous companies have, in multi-billion-dollar transactions, taken ownership of onshore IOC assets in the Delta, which represents a historic moment for Nigeria and Sub-Saharan Africa’s oil and gas industry. In Senegal, Ghana and Côte d’Ivoire, upstream activity is accelerating. Eni launched Baleine Phase Two in Côte d’Ivoire, tripling oil production. Jean-Marc Kloss, SLB West Africa’s managing director, said: “One of the most significant projects in West Africa is Eni’s Baleine development in Côte d’Ivoire, which is Africa’s first net-zero upstream project. Beyond Côte d’Ivoire, SLB is involved in multiple high-profile projects across Ghana, Equatorial Guinea, Nigeria, Mauritania and Senegal.”

Despite the inherent challenges in West Africa, upstream development across the region unlocks opportunities for regional midstream and downstream development, strengthening energy security in an area with high levels of energy poverty. Mohammed Mijindadi, president of GE Vernova, Nigeria & managing director, Anglo-West & Francophone Africa, said: “Senegal, for example, having recently discovered gas reserves, is enhancing energy security and establishing itself as a regional energy hub.”

Natural gas projects are taking off across Sub-Saharan Africa. The resource is highly sought after in export markets and can foster domestic industrial development as a cheap, abundant source of energy. Mansur Mohammed, head of new business development Africa at Wood Mackenzie, said: “The rise of Floating LNG (FLNG) projects positions Sub-Saharan Africa as a global leader in this area. Cameroon, Congo, Senegal and Mauritania have FLNG projects, and others are developing theirs.”

Global markets dictate oil and gas developments in Sub-Saharan Africa as much as local developments. Charles Lowery, country manager and director of TEST Angola, said: “The foremost challenge remains the volatility of Brent crude prices. Short-term factors such as tariffs, global trade dynamics, the US political landscape, and Chinese demand influence market conditions. This volatility places pressure on investment flows, making capital allocation highly competitive. Paradoxically, the volume of tenders TEST Angola is bidding on is higher than ever. Despite the downturn in oil prices, this environment presents new opportunities for service providers, especially in mature markets like Angola where outsourcing services has become more cost-effective than in-house execution by the IOCs.”

Indeed, in South Africa, Angola and Namibia continue to attract attention. Angola’s upstream sector is maintaining production levels, and its regulatory entities have pushed for the onshore space to receive more attention. As natural production decline continues, further exploration work will be necessary, and small and mid-sized Independents will have to be drawn in to reinvigorate mature assets as IOCs transition to greener pastures. Those greener pastures in Africa find themselves further south, in Namibia. With a new president, the country is overhauling its oil and gas regulatory structure, as investors watch closely. Despite recent changes, discoveries continue to pick up the pace, and new players are entering the market, triggering an influx of international and African service providers into the country. The country’s coastal ports, at Walvis Bay and Lüderitz, are undergoing historical transformations, as will Namibia’s economy once the first oil is achieved.

Namibia’s financial establishment is readily adapting to the new oil & gas paradigm, but the deep need for both capital and time in long-term energy projects still presents a challenge. Rachel Mushabati, Senior Associate Attorney and Country Head: Namibia at CLG said “The local financing landscape is still unprepared for large-scale energy projects. Most of the financing still comes from international banks, export credit agencies, and private equity due to the sector’s high capital demands and associated risks.”

At the local level, the multi-faceted needs of a nascent oil & gas industry, including infrastructure development and human capital formation, are being confronted with financing constraints. Veronique Herman, CEO of Africa Provider Offshore Services (APOS), which provides training and certification services, said “Local companies need access to financial institutions that truly understand the specific challenges and opportunities of the oil and gas sector. We need banking partners who can evaluate projects holistically, respond quickly, and move beyond traditional models.”